Last Bites: Closing Time for Drizly and for Low Interest Rates

They don’t have a home to deliver to so I guess they have to stay here? Uber is shutting down the alcohol delivery service it acquired for north of $1.1 billion to fold it into the main UberEats app. There were other issues with Drizly, and the company line is that Uber wanted to deliver everything under one brand, but to shutter a $1B acquisition dovetails with a larger market shift that can be constructive to small business owners.

For as long as most people have been in business or can remember, interest rates have hovered around zero percent. The more recent raising of interest rates by the fed has been viewed as an anomaly, when if you widen your lens it’s the rock-bottom interest of the past 20 years that are anomalous.

If we assume that higher rates are here to stay – what does that mean for restaurants?

1. Loans are going to be more expensive.

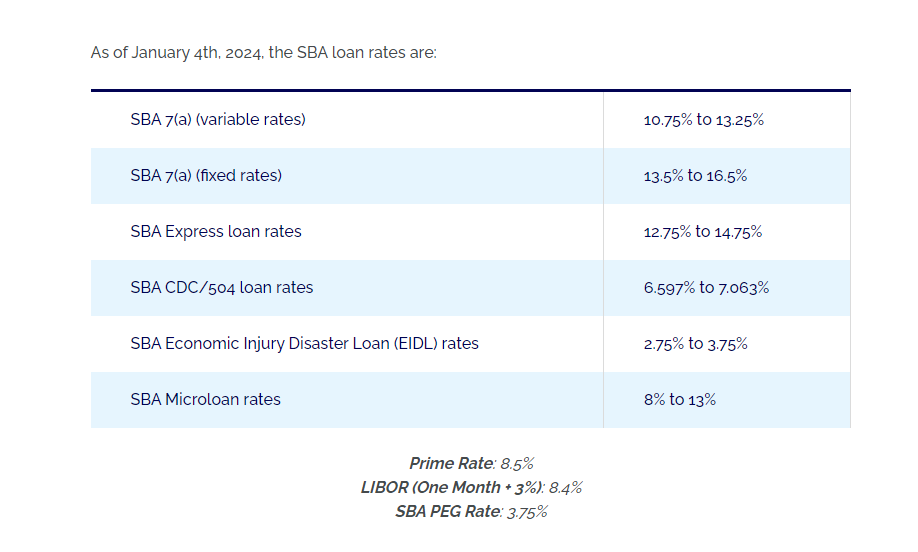

Most loans are “fixed rate” or “floating rate” loans meaning that a borrower pays the same interest rate for the life of the loan (fixed) or that the borrower pays a rate depending on a benchmark interest rate (floating). In the floating rate model it’s easy to see that higher rates will affect the benchmark rate and go up. But even fixed rate loans are traditionally benchmarked to a rate so you can expect to be paying north of 10% interest.

2. Equity is More Expensive as Well.

Investors, even those friends and family types, are best thought of as providers of money – who are (usually) looking to balance the risks of an investment with the upside or money making potential. A core principle in investment is the need for a balance between risk and reward. Currently, traditionally "risk-free" investments such as U.S. Treasury bills and top-tier corporate bonds have seen their costs increase alongside rising interest rates. Those who have money, like banks looking to make loans, have the ability to get higher interest rates for their cash. For sophisticated investors this means that they will demand higher returns on their investments. Any possible new ventures should be prepared to make do with less equity capital if they are planning on delivering an acceptable return.

3. Real Estate Leverage Becomes Critical.

And we don’t mean the importance of choosing the right location because that is always critically important to success. What becomes critical is the ability to save money / gain leverage on the capital you are bringing to the real estate process. There are two ways to do this: 1) find a second generation space to allow you to save dramatically on build out costs or 2) leverage your brand equity to secure money from the Landlord to invest into the space (called “Tenant Improvement Allowance”) or TI. Both options will likely increase your rent per square foot but will lower the amount of capital needed to be raised or paid back.

4. Make Sure You Are Getting Interest.

Many of our clients often have significant cash in the bank as either cash reserves or awaiting distribution. While that could just sit in a non-interest bearing account in the past if you’re doing that now you are losing out on possible cash. There are checking / savings accounts that are FDIC insured that are offering 3-5 % interest on deposits. Let’s say you have a restaurant that makes $2M a year with 10% margin and keep $150,000 in a reserve account. Assuming you make a once yearly distribution to investors you would have $350,000 that you could be earning interest and at a 4% rate equaling up to $14,000. The timing of deposits would work differently but it’s either way it’s a lot of money! You could increase profits up to 7% by doing nothing but changing bank accounts.

These are 4 things to be conscious and managing, no matter how long this new paradigm lasts. We certainly hope that interest rates lower to help small businesses but it never hurts to be efficient with your money.